Harbor Diversified (OTC: HRBR)

Written on July 12th, 2021

Disclaimer: This is not financial advice – please do your own due diligence.

Author’s note: This is one of the most intriguing, and possibly most asymmetric risk/reward special situations that I have ever seen. As a result, I have made HRBR a significant position in my portfolio at $2.0/share.

Situation Overview

Harbor Diversified (HRBR) is a shell company for Air Wisconsin, a regional carrier for United Airlines. Air Wisconsin services primarily the Midwest area with short routes with a fleet of 64 Embraer CRJ-200 50-seater planes.

The regional carrier business model is generally seen as more favorable than the traditional airline business model. Large airlines, such as United or American, will contract with smaller regional players, using what is called a capacity purchase agreement (CPA). Air Wisconsin’s single and only client is United Airlines, and their CPA currently runs with them through Feb 2023. Through the capacity agreement, Air Wisconsin provides the planes and their maintenance, the flight and cabin crew, for which Air Wisconsin receives a fixed payment for each aircraft and each departure and block hour flown. United, on the other hand, manages all the operational side of the business (ticketing, pricing, etc.) and lets Air Wisconsin use the United logo on their planes. These contract payments due to Air Wisconsin are generally paid up-front at the start of the year, so the fixed nature of the contract with the regional carriers is generally disaster-proof, evidenced by the fact that HRBR’s revenue during 2020 was only down 30%, which is small relative to United’s steep 65% revenue drop in 2020. Air Wisconsin also now owns all their planes, so there are no fixed rent costs that could harm them in a disaster scenario.

Don’t worry - I’m not about to pitch a vanilla, undervalued regional aircraft carrier trading below book value. HRBR’s situation got extremely interesting on June 29th, 2021, when United Airlines had an investor presentation where they showed the following slide:

Following the release of United’s presentation, HRBR’s stock tanked 40%, from $3.08 to $1.87 on fears that United was phasing out its entire fleet of 50-seater planes, which are precisely the only type of planes that Air Wisconsin flies. A first-level line of thinking would lead you to believe that United was not renewing their CPA with Air Wisconsin past February 2023, so the stock should be priced as a going concern only through that date.

However, after opting for a second-level thinking approach to understand the complicated narrative surrounding this asset, I am convinced that it is likely that United will in fact extend its CPA with Air Wisconsin, making these liquidation fears overblown.

Let’s go over a few key points to illustrate the point that United is not ending their relationship with Air Wisconsin, and in fact, likely renewing their agreement with them.

CPA Amendment

In October 2020, United amended their CPA with Air Wisconsin to include a call option to extend their agreement from its expiration in February 2023 for no less than two years, but not more than three years, in which case it would expire between February 2025 or February 2026. Additionally, United added yet another call option to extend the agreement for an additional two-year period following the expiration of the extended agreement, in which case the CPA would expire between February 2027 and February 2028.

Remember that the positive vaccine news that provided a rising tide for the airline industry were not announced until November 2020. In fact, in July 2020, United announced that they were not renewing their CPA with ExpressJet, another one of United’s 50-seater regional carriers. Common sense would lead me to believe that United would not have even bothered to add a call option to the CPA if they were going to effectively kill an airline in what was still the middle of COVID, which would have been a perfectly reasonable time to do so.

New CFO

Liam Mackay is the current CFO of Air Wisconsin, a role he just recently signed up for in January 2021. Before joining Air Wisconsin, he was the director of United Express Commercial Strategy, a position he attained after being a United employee for 10 years. Why would he leave a stable and cushy job at one of the largest airlines in the US to join a regional airline that was about to liquidate? Remember that the move also includes uprooting his family from Chicago, Illinois to Appleton, Wisconsin. Seems strange to go for all this trouble for a two-year stint. Bear in mind that he was the director of United Express’s strategy – he probably knew that Air Wisconsin was going to be one of the beneficiaries from United’s five-year corporate plan.

Buyback program

On March 31st, 2021, management included a plan where they were allowed to buy back $1 million of stock a month, ramping that up by $1 million every month thereafter. Now, bear in mind that the total fully diluted market cap of the company is $140 million!

It’s worth noting that they have not bought any stock since their latest quarterly report as of 3/31, but why put the plan in place if you are not going to use it?

United’s Fleet Composition and Strategy

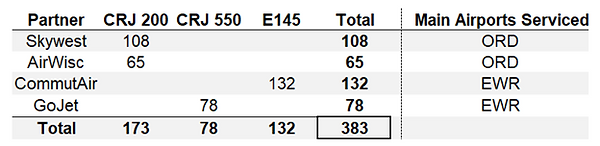

Let’s dispel the myth that United is getting rid of all of its 50-seater planes – the slide shown previously clearly states that United is getting rid of 200+ 50-seaters, not all of its 50-seaters. If we compile each of United’s regional partners’ planes from their respective quarterly reports, we see that United actually operates 383 50-seater planes.

The conference call audio (not the deck) provided key pieces of information that allow us to back into Air Wisconsin still being a United partner by at least 2026 by process of elimination.

Piece 1: “Here in Newark, we still fly. And Newark is our largest gateway -- largest hub in the East Coast. We still fly a ton of single-class RJs, 27% of the operation. We're going to take that to 0 by the end of this year [2021].”

Air Wisconsin doesn’t cover Newark, so it’s safe there. GoJet is also safe since their C550s are triple-cabin, not single-cabin. That leaves CommutAir’s 132 E145s to be phased out.

Piece 2: “We're trying to fly 50-seat regional jets between Chicago and Dallas or between Newark and Atlanta.”

This confirms that GoJet is safe as Newark is one of their main hubs.

Assuming that GoJet is safe and CommutAir is getting phased out, that leaves Air Wisconsin and Skywest to figure out. Recall that the deck said that they were phasing out 200+ 50 seaters. If all three airlines were cut, United would have specified that they were phasing out 300+ planes instead (132 + 65+ 108 = 305). The likely conclusion from this is that Skywest and Air Wisconsin will continue being United partners, albeit with reduced capacity, at least through 2026.

Piece 3: “Our hub in O'Hare, ORD, on this slide, 42% of our departures are single class RJs. Our biggest competitor in O'Hare is only 28% and that number is going down. And then in Minneapolis and Detroit, close by, the number is 18% and 19% and likely headed close to 0 over the next year or 2. So we're going to take 42%, and we're going to reduce it down to 4%. It's going to be a marked change about who United is in Chicago by 2026”

United needs Air Wisconsin, as it provides a valuable service to its customers and its Midwest expansion strategy. It simply does not make sense for United to not renew the CPA with them given what was outlined in their presentation.

Incredibly Experienced and Aligned Management Board

The board is a majority and controlling owner as it owns 51% of the outstanding equity. These are experienced aircraft operators that have held and managed airlines for most of their lives.

The history of HRBR should paint a better picture of the board’s savviness. In 2010, Harbor was an unprofitable biotechnology company about to go bankrupt. Amun (the name of the entity controlled by the board) put up $2.8M to own the entity’s NOLs (net operating losses) to ostensibly offset them against future gains.

So, they bought HRBR, sold Air Wisconsin to the HRBR shell, took over the NOLs, and did a reverse stock split to bring its total number of shareholders to under 300 (which is the maximum number of shareholders that you are allowed to have before you are legally obliged to issue public filings), and delisted from major exchanges and went dark for 10 years. It is common for companies to go dark to avoid filing and audit costs.

However, in April 2020, a shareholder noticed that HRBR had crossed the 300-shareholder threshold and reported them to the SEC, forcing them to issue their first public filing in 10 years. The filings revealed a cash-rich and profitable entity that attracted a lot of attention, with the shares climbing from $0.10 all the way to $3.10 before United revealed their new five-year plan.

Being majority owners, I fail to see how a board this experienced and incentivized can choose to liquidate an asset that has been incredibly lucrative for them for the past ten years.

Hopefully, the points above dispel any fears that United will not renew Air Wisconsin’s CPA.

Valuation

Let’s talk about HRBR’s current valuation - it has a relatively simple capital structure:

54,863,305 basic shares outstanding, plus

16,500,000 diluted shares from convertible preferred shares, plus

558,835 options exercised at $0.214 (~500,000 diluted shares using treasury method)

Equals ~70,000,000 fully diluted shares

At a current share price of $2/share, this brings HRBR’s fully diluted market cap to $140 million.

But subtract:

$170m in cash and receivables

And add:

$204m in debt, payables, and deferred revenue

To arrive at a total enterprise value of $174 million.

Let’s consider the scenario where HRBR gets liquidated in February 2023 to understand the context of the absurdity of this valuation:

Reversing a DCF through February 2023 using a very conservative $25 million yearly FCF assumption, we get to the current $2/share price. This is an EXTREMELY conservative assumption considering the fact that this business is slated to clear $30-$40 million in FCF in 2021. HRBR is also expecting an additional $53 million from the Payroll Support Program in 2021, which is not expected to be paid back to the federal government. This means that in 2021 alone, HRBR is expected to clear >$100 million in FCF, more than half of its current enterprise value.

The point of this exercise is to show that this setup provides investors with a classic ‘tails I don’t lose that much, heads I win’ setup. If you invest in HRBR today, and it underperforms by only generating $25 million per year and gets liquidated in 2023, you get your $2/share back – not bad.

As I’ve made clear, however, I think that this is very unlikely to happen. The likely scenario is that United renews their CPA with Air Wisconsin, causing the stock to significantly re-rate upwards to $3-4/share to reflect an additional 3-4 years of additional cash-generation.

Risks

There are two risks that I see with this investment, both surrounding the controlling entity.

First, given that they have gone dark in the past, there is a risk that they could do this again and leave minority shareholders hanging. This risk is mitigated by the fact that given that they have reported a 10-K and a 10-Q this year, they are forced to continue to do so at least until the end of the year. More importantly, they have long breached the 300-shareholder of record minimum threshold. I seriously doubt that they will be able to go dark again anytime soon.

Second, there is the possibility that management pays out a dividend to the preferred shareholders, which are conveniently owned by the controlling entity. I do not see this as a huge risk in the near term for two reasons. First, PSP covenants prevent them from paying a dividend until at least April 2022, so it is not a near-term risk. Second, this is a lucrative enterprise that they have controlled for 10+ years, and given a possible fleet expansion in the near future, it does not seem reasonable to liquidate the entity.

Conclusion

Liquidation fears for HRBR are overblown – and I hope that I have convinced you of that. At $2/share, you are buying a free call option with significant upside to a special situation that sold off after a cursory understanding of the situation.